Coronavirus and bankruptcy: What you need to know

Americans are facing challenging times wrought by the coronavirus pandemic and the aggressive measures to fight the curb the spread of the disease.

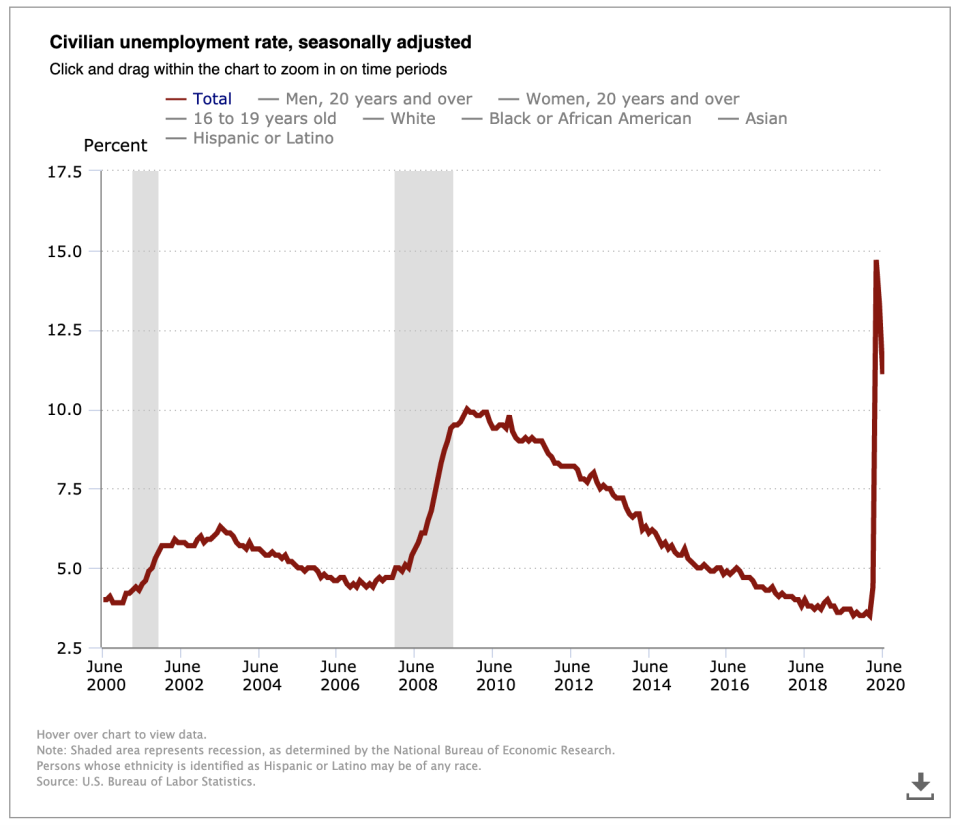

Since March, tens of millions of workers have lost their jobs, while companies big and small have gone out of business. A surprising development is that the number of Americans filing for bankruptcy has dropped steeply during this time.

Bankruptcy attorney Gregory Wade from Alexandria, Virginia, joins Cashay’s latest Money, Honestly podcast to discuss the decline in bankruptcies, what he expects as the pandemic continues to hurt the economy, and what every person should know about filing for bankruptcy.

The podcast episode is based in part on the reporting from the Yahoo Money article: “Personal bankruptcies plunge during pandemic, but 'a flood' could be on the horizon.”

Janna: Hi, this is Money, Honestly. I'm Janna Herron and today Gregory Wade, a bankruptcy attorney in Alexandria, Virginia is joining us. We'll be talking about bankruptcy during the coronavirus pandemic. Also help us understand what you should be thinking about if considering personal bankruptcy. Thank you Gregory for being here today. Let's start out by discussing the state of bankruptcies right now, especially given this really unprecedented time. What are you seeing?

Gregory: Hi, Janna, it's nice to be here. Right now, today, as we speak, we are seeing a surge in commercial bankruptcies, but not yet a surge in consumer bankruptcies. Consumer bankruptcies, and all bankruptcies have actually been down for the past 12 months because the economy been doing so well, there's high employment, people have plenty of money, but the coronavirus and its devastating effects on the economy, they're really hurting business and they're the first ones to file bankruptcy today.

Janna: And you said some of the bankruptcy courts have been closed because of the pandemic. Does that have anything to do with any backlog?

Gregory: It's not so much that the bankruptcy courts have been closed. I think you've always been able to file a petition, but what happens is the other courts, the state courts have been closed or have dramatically reduced their ability to handle work. So what that means is that if someone was facing, say a foreclosure or an eviction, the landlord could not evict because they were either prohibited by law from evicting or the courts were not available or understaffed. So there've been very, very few of the kinds of legal trouble that propels people into bankruptcy.

Janna: I got you. So you're seeing the business side, there are lots of bankruptcies, not so much when it comes to individuals. Is that because a lot of individuals, maybe who've lost their jobs are getting a lot of support right now from the government.

Gregory: Yes. That's correct. They're getting unemployment, which I think is supposed to run out at the end of this month, if I'm correct. And in many cases-

Janna: Yes, that extra $600.

Gregory: Yeah, exactly, Janna. And they're also benefiting from the fact that the courts have slowed and they're not being pushed into it.

Janna: So what do you expect for bankruptcies? And when I'm talking about bankruptcies, individual bankruptcies going forward in the fall and the winter, especially if the federal government doesn't extend those unemployment benefits you were talking about, or maybe doesn't send out more stimulus payments.

Gregory: Well, assuming that Janna, that's an excellent question. And of course, when you're trying to predict the future is always risky, but I expect that there will be an avalanche of consumer bankruptcies. Remember, every time as unemployment rises bankruptcies go up, because people can't pay their bills and we're already seeing a tremendous number of evictions happening. I know in Texas, the evictions have just skyrocketed. And every time there's an eviction filed, it is a potential bankruptcy because people don't want their belongings and themselves put out on the street. And if they don't have enough cash to go and put a down payment or a deposit on another apartment, they're stuck.

Janna: Right. Right. So that sounds terrible. So there is a real potential for all these people who may have lost their jobs or their incomes to be stuck in a situation where they might need bankruptcy. So how does a person know if bankruptcy is something that they really should consider?

Gregory: Well, that's a good thought and a good question, Janna. It somewhat depends on the person. I once knew an Episcopal priest and he said that, "The world is divided into two kinds of people, those that divide people into two types and those that don't." So I'm going to divide people into two types. There are one, the more financially sophisticated people, those that keep track of their money, watch what they do, that they file bankruptcy too, but they usually see it coming. They a little more prescient than others.

Some people, and it doesn't matter really how wealthy they are, but if they handle their money and their assets in kind of a slipshod way and don't pay a great deal of attention to it, they don't see it coming. So the people that see it coming are able to get bankruptcy counsel early on, and there's a tremendous amount that can be done for them to minimize the effects. Those that usually are forced to see a bankruptcy lawyer by some external event, like a layoff, a divorce, a lawsuit, a foreclosure and eviction, they're suddenly facing this problem [inaudible 00:06:24].

Janna: And that external event probably will be something that happens for a lot of people this time around given that they suddenly lose their job because of this pandemic. Is that correct?

Gregory: No question. I mean, look at the unemployment today, compared to the unemployment pre pandemic. I think you can look at every single person who received unemployment in the past three or four months, and there's millions of them. Every one of them is a potential, has a potential bankruptcy in the future, unless they're able to find another job and there's no economist that thinks that employment is going back to what it was pre pandemic.

Janna: Right. That's very frightening, but that's why I wanted to talk to you about bankruptcy, because I think a lot of people, when they think about bankruptcy it sounds like a very scary nightmare situation and they have a lot of concerns, questions, and worries going into it. So I thought maybe you could help break down those things and still it might not seem as scary. So what are some of the common questions or worries people have when it comes to bankruptcy when you talk with them?

Gregory: Excellent point, Janna. Probably the most common sentiment is that of embarrassment, and guilt and shame. I think that applies across the board, no matter what a person's socioeconomic background is and what I tell them is that what they have to realize is that bankruptcy is there for a reason. It is constitutionally based, article one of the constitution, even before the Bill of Rights [inaudible 00:08:34] the Congress shall make uniform bankruptcy laws, and it is also biblically based in Deuteronomy, I think it's 15. It says that, "Debts shall be discharged every seven years." So the fact that you're having financial troubles and that you're turning to the law or the government for help is something that people have been doing for eons and eons. So the first issue we face is how to make them look at it rationally and set aside the fear and the shame at least to hear what they can do.

The second thing they have is they want to know about their credit. How's it going to help my credit? How's it going to hurt my credit? And bankruptcy is odd in terms of law because there's so many things that are counter intuitive. I sometimes say, it's like when you in grammar school and you learn negative numbers. You realize when you add up negative numbers, the addition produces a smaller number and when you subtract negative numbers, the subtraction produces a bigger number. So it's just the opposite of what you would expect. And there's a lot of that in bankruptcy, especially in credit, because credit many, many times is helped by bankruptcy, not hurt by bankruptcy. And yeah, [crosstalk 00:10:21] it is counter intuitive because the way it functions is that bankruptcy itself is a black mark on your credit, but it is not nearly as black as owing a ton of money because it helps your credit in the sense that it cleanses and takes away the debt.

So if you make X number of dollars per year, and you owe a ton of debt, you have no credit. If you make X number of dollars and have no debt because of bankruptcy, you do have the ability to have credit. And there are some credit card companies that will send you application for credit card knowing that you filed bankruptcy. So that helps people's credit. That's the second big thing that they ask you the first. And I guess the third is, I want to buy a house, how can I buy a house? Is it going to ruin me for life? And the answer is, no. Most Freddie Mac and Fannie Mae and Veterans Administration really are involved in most of the consumer residential home mortgages and they like you to wait two years after you filed bankruptcy and then you're eligible to apply. Now, it depends upon what you've done in those two years. Are you back in debt or have you handled your life well and paid your bills and established credit, but after two years, you're back in the housing market.

Janna: Wow. Okay. Well, that's really a relief for a lot of people.

Gregory: What is another thing, we're in the Washington D.C. Metropolitan Area and so many of the people that work here have security clearances, and they are worried about the security clearance. Am I going to lose my job? And I can say categorically that, and I've done hundreds of these, I've never seen a person lose a security clearance because of a bankruptcy. Now, sometimes what'll happen is if the bankruptcy was caused, for example, by gambling or drug use or some other underlying problem, the bankruptcy might bring that to the fore and result in it. But simply because you overspent, nobody loses their security clearance for that. As a matter of fact, you can argue in the same way that it helps credit, you can argue that a bankruptcy helps security clearance, because if you don't know owe money, you're less likely to sell secrets to somebody that shouldn't have them if you have a security clearance. And if everybody knows that you're bankrupt, you're not a risk anymore. So those are the misconceptions that we face on a daily basis.

Janna: That's really interesting. Thank you for going through all of those. We also had talked previously about some of the worst mistakes people make leading up to a bankruptcy. I'd like to go through those because someone who's considering bankruptcy who might be listening, might be thinking, "I should do this," when maybe they shouldn't be doing it.

Gregory: Yeah, that's another common question and a good point. I guess the most common mistake is they wait too long. They don't want to file bankruptcy and we appreciate that they don't want to do it. These are honest, hardworking people that are holding down jobs and homes and supporting other people. They don't want to file bankruptcy. So they wait. But during that time, they oftentimes deplete all of their assets that they could have saved in bankruptcy. And one of the most common is a borrowing against, or closing out retirement accounts, like a 401k or an IRA, or some other of retirement accounts that the government have, Thrift Savings Plans, because those are exempt from bankruptcy.

And what they do is they don't want to come in, they don't want to do it, so they borrow against the 401k. They still wind up filing bankruptcy, but they've lost their 401k when they have drastically reduced it and diminished it. They could have come out with $100,000 in a 401k from bankruptcy, but instead they still file bankruptcy and come out with $60,000 in their 401k, they literally threw away $40,000. And the last most common one, I think is they try to hide their assets. They think, "Oh, I'm going to put my car in my brother's name," or, "My sister and I inherited a house when our parents died and I'm going to just give my share of the house to my sister." That's a terrible thing to do. Absolutely terrible because the bankruptcy court sees that. So not only can it be undone, but it looks as if you're being too cute and you're attempting to defraud, and it can prolong the bankruptcy and make people look at it a little bit harder than they might otherwise do.

Janna: Those are really interesting points. I would like to go over the 401k bit or the retirement savings bit just really quick, just to make sure everybody understands this, because I think it's an important point. So if I had a whole bunch of credit card debt or medical debt and I'm trying to pay it down, I'm struggling and I'm like, "well, I'm going to just tap into my 401k because there's a whole bunch of money in there and use some of that to hopefully pay some of this down." And I do that and then it doesn't work. I still owe a whole bunch of money and I file for bankruptcy, but now my retirement account would have been safe in bankruptcy, but now it's a lot less. So I'm a lot less secure. Am I getting that?

Gregory: That's exactly right. That's well put.

Janna: Wow. So that's really interesting. I don't know if people were aware that their retirement savings are shielded in bankruptcy and that's really helpful because that's your future financial security right there.

Gregory: Yeah. The purpose of bankruptcy, a lot of people don't understand the purpose. The purpose of bankruptcy is to give people a fresh start, it's not just because it's a humane thing to do to help people, but it also helps the economy. Because if you get somebody who's mired in debt, every time they start a bank account, it gets garnished, they can't rent an apartment, they can't buy a house, they can't save anything, they wind up working under the table and not paying taxes. So for an individual, what bankruptcy does is that transforms someone who would be an economic burden to society. It transforms them into an economic asset, a tax paying citizen, who's raising children, paying rent, buying cars, doing all of the things that we all do in the economy to make it strong.

Janna: That's a really good way to look at it. I never thought about it that way, but there's a bigger purpose to it, not just your individual purpose. I think people also worry about if they already own a home and they go into bankruptcy, what are the options there?

Gregory: Yeah. Well, there's a lot that you can do and that's dependent on a couple of different facts. One important fact is, what state you live in. You see, bankruptcy is a blended area of law. It's blended with federal law, which is the federal Bankruptcy Code. And remember the constitution says that, "Congress shall make uniform bankruptcy laws," and Congress did as they are required to do. They made these laws. But the exemptions from bankruptcy, that is those things that you can keep, even in the event of bankruptcy are dependent upon state law. So different states have different approaches to what property is exempt. And when we say exempt, we mean exempt from the claims of creditors. And in some states your entire home is exempt, most particularly in Florida and Texas. So there's no amount on it.

You can have a $5 million home in Texas or Florida and file bankruptcy and the home itself is untouchable. There's another way in which assets are untouchable. For example, in Virginia and Maryland, all around in many, many states, there's a concept called tenants by the entirety. This actually goes back to the middle ages. And the notion was that when a husband and wife were married, I'm talking about the middle ages, not today. Today it would also apply to same spouse marriages as well. But initially, when two people were married, the notion was, is that there was a new spiritual entity, which is neither completely the husbands nor completely the wife.

So if they owned property and it was titled as tenants by the entirety, that's so much like magic language, then what that means is that only the debts of both spouses can be used to satisfy to cause the sale and the liquidation of an asset that is held by tenants by the entirety. So it's completely different. So in your bankruptcy planning, what you do sometimes is what we advise people to do is you say, put the assets and tenants by the entirety and keep all the debts and individual names. So therefore, [inaudible 00:22:13] up and never the twain shall meet. So somebody can file bankruptcy and have a ton of money in a house even if the homestead is very small, but the home itself would be exempt because it is tenants by the entirety.

Janna: Interesting. All right. So basically the people... depending on your state, you have different ways of possibly protecting your home and bankruptcy.

Gregory: That's correct. And right now we've been talking about Chapter 7, there's also Chapter 13’s. Chapter 13’s are kind of uniquely designed for homes and that can be protected too, but that's more of a reorganization plan rather than liquidation plan.

Janna: Got you. And what if I'm considering bankruptcy and I have some money in my bank account, lump sum that otherwise it's probably going to go to creditors, but before I file for bankruptcy, is there something I can do with that money to protect it or shield it in a up and up kind of way.

Gregory: Yeah. And there's a limited amount that you can do. But what you can do with that is, the first thing you can't do with it is give it away. Change the account and give it to you, give it to a good friend or a family member. You can't do that. That's that's really fraud. But what you can do is you can spend it in such a way that it does not increase your net value. For example, a common example is dental work. One of the things people do is that, especially if they're having tough times, they put off going to the dentist and sometimes people come in and you can just look at them and say, "You really need to go to a dentist."

Well, we say, "We try to be as gentle as we can, but it's something you should consider." But people, they sometimes can have $20,000 in the bank and they're saving it, and they would lose it in the bankruptcy. I would say, before you filed the bankruptcy, get your dental work done. And they go in and spend $15,000 on dental work and you can't take that away from them. The court's not going to pull your teeth out.

Janna: Hope not.

Gregory: And another thing you can do is you can use it. Let's say you own a house that is exempt and you need a roof. I wouldn't suggest doing it if you didn't need the roof. But if you need a roof, then put the roof on the house, you've been putting it off because times are tough. But that roof on the house, you might get a new washing machine and dryer. There's other things that you can do which will not increase your net worth, so therefore make it harmless in bankruptcy, yet you can use that money in a way that makes your life easier.

Janna: That's really interesting. When we spoke previously, Gregory, you also talked about the way to keep someone or keep a credit card after bankruptcy and I thought that was really interesting. Can you go over that?

Gregory: Yeah, Janna. This is among the services that our bankruptcy counsel offer is, his way not only to get out of the financial problem that you're in, but to restructure things so that going forward, you'll have it a little better. And we talked about buying a house. You can buy a house, after two years you're eligible, but you have to have a decent credit rating. And one of the problems with bankruptcy for some people is that they find it hard reestablish credit. Or one of the things you can do is, if you have credit card that has a relatively low balance, and some people they have tons of credit cards. Every time they get an application, they sign it and say, "Yes." So they come in and they have dozens of credit cards.

Some of them haven't been used or some of them have been used. So you pick one out that you can use you. I advise people to use it once, make a small purchase, $15, $20 purchase, and then pay it off just to kind of activate it and then you file bankruptcy. And if the balance that you owe on that credit card is zero, it does not have to be included on your bankruptcy. You must include all your debts, it's no longer a debt. Now ou can't do that with huge big amount, but then you can emerge from bankruptcy with a credit card. And some people can actually go and apply and get another one and then file bankruptcy. But you have the credit card, but it's a zero balance and it helps you to do things like buy things online, and rent a car and do stuff where you need credit card.

Janna: That's really... that's smart. And like you said, that will help you as you go forward from your bankruptcy to build your credit and start doing those things that you might want to do, like buy a house two years down the road. Thank you, Gregory. This has been a really interesting conversation and it really highlights what people probably don't realize about bankruptcy and talking with a professional like you. It really is helpful for them and may make the bankruptcy process a lot less scary. So thank you Gregory for joining us today on Money, Honestly, and thanks for everyone listening. Head over to Apple Podcasts and leave us a five star rating and review. We'll see you next week.

Gregory: Thank you, Janna.

Janna is an editor for Yahoo Money and Cashay, a new personal finance website. Follow her on Twitter @JannaHerron.

Read more information and tips in our Debt section

Read more personal finance information, news, and tips on Cashay